‘Money makes money. And the money that money makes, makes money’ – Benjamin Franklin

In 2018 the average 20-year-old has a lot to complain about when it comes to money…

The house price to income ratio is at an all-time high, wage growth is below inflation and you’re lucky to get 1% in a savings account.

Yet! Without much effort or education, these same 20-year-olds can achieve investment returns financial professionals with decades of experience can only dream about.

Take a look at the following three scenarios:

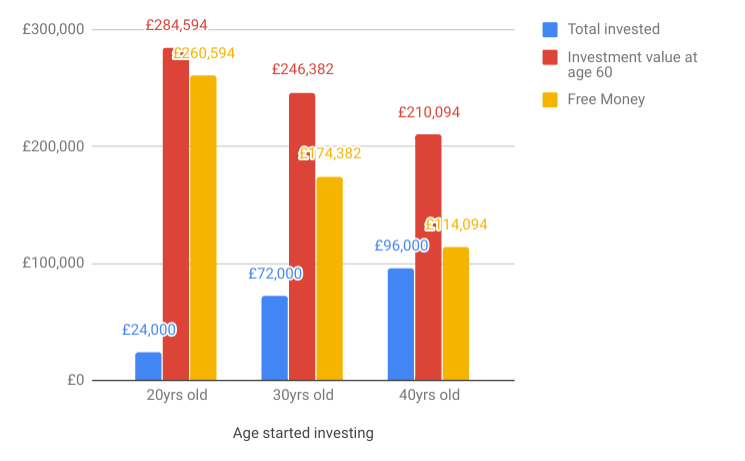

Assuming an investment return of 7% who do you think at age 60 ends up with most?

Answer = The 20-year-old even though he invested 200% less than the 30-year-old or 300% less than the 40-year-old!

Below is a graphical representation of this:

In particular, take a look at the free money bar, the 20-year-old earned £260,594 in compound interest whilst the 40-year-old ‘only earned’ £114,094 despite investing 300% more.

So how is this is possible?

The answer is: Compound interest

The principle behind this is that if you keep the interest your money has earned invested you then make extra interest the following year since your overall balance has increased.

This is explained in the following table:

| Year | Start of year balance | Interest rate | Interest earned | End of year balance |

| Year 1 | £100 | 7.00% | £7.00 | £107.00 |

| Year 2 | £107 | 7.00% | £7.49 | £114.49 |

| Year 3 | £114 | 7.00% | £8.01 | £122.50 |

| Year 4 | £123 | 7.00% | £8.58 | £131.08 |

| Year 5 | £131 | 7.00% | £9.18 | £140.26 |

Note: The interest earned increases each year despite the interest rate staying at 7%.

The interest continues compound each year (hence the name Compound Interest) and is an insight into how longer investment periods allow for greater returns.

This is how the 20-year-old in the first example managed to invest ‘just’ £24,000 yet end up with a balance of £284,594 a ROCE (return on capital employed) of 1185.81% vs the 40-year-old who invested £96,000 to achieve a balance of £210,094, a ROCE of 218.85%:

| Age Began Investing | ROCE | Years Invested | Annualised return |

| 20-year-old | 1185.81% | 40 | 29.65% |

| 30-year-old | 342.20% | 30 | 11.41% |

| 40-year-old | 218.85% | 20 | 10.94% |

Look at the difference in the annualised return (ROCE / years investing) since the 20-year-old was invested for so long he achieved a 29.65% return per year despite only ever earning a 7% annual interest rate.

This is the premise behind how a 20-year-old can set and forget his or her investments and earn a return beyond the dreams of a 50-year-old financial professional.

Additionally, don’t forget many investment benefits we now take for granted simply didn’t exist a generation or two ago:

You used to have to pay serious amounts of money just to buy shares (and this remains the case in many countries).

Index funds are a relatively new phenomenon only opening up to investors in the 1970’s.

The investment ISA allowance has never been so high! A huge benefit many international investors look on with envy.

Add these advantages on top of compound interest and it becomes clear investing should begin as soon as possible in order to fully harness the benefit.

Despite the benefits, only 5.42% of the UK adult population have an investment ISA (based on 2.6 million having a stocks and shares ISA in 2017 and 28m 20+ year olds living in the UK).

Why is this? Partly I think it’s due to little education occurring in school on the benefits of investing (teachers are simply too busy with rigorous reporting and the school curriculum) and partly to the hangover that you need ‘lots of money’ to start investing…false!.

Finally, I think many of us see a 7% return as very unsexy and not worth our time. Take for example the boom in Cryptocurrency.

The Independent recently claimed 1 in 3 millennials invested in Crypto in 2018. A figure WAY higher than the previously mentioned 5.42% that have an investment ISA, now ask yourself if Cryptocurrencies were returning 7% a year would these same individuals invest in it?

I’m not saying you shouldn’t invest in it, just that it’s incredibly volatile and it’s technology and concept so recent you maybe more likely to lose most of your money compared to an unsexy index fund (see below for an explanation).

Yet, if they did invest in the index fund that returned 7% on average year after year and held onto it for decades, over the long-term it may well provide returns far higher than cryptocurrency.

Since I’m not a licensed financial professional and we’ve likely never met I can’t answer this question directly read on…

What I can say is assuming I’m investing for a long time period equities (stocks and shares) remain my favorite choice.

The easiest way to invest is through buying an index fund (a fund is simply a pool of individual investments) that captures the return of a stock market.

An example fund could be the ‘FTSE All-World Index’ which aims to capture the movement of global stock market performance by investing in 8,000 stocks across 48 countries.

This way I avoid the high risk of investing in individual companies or countries (Brexit!).

Or if I’m after less risk with slightly less returns I can de-risk my investment by additionally investing in Gold which typically has an inverse correlation with equities (read How To Own The World for more information on this strategy).

Furthermore, by investing the same amount every month I can turbocharge my returns through the power of pound-cost averaging (you smooth your returns by buying less when it’s expensive and more when it’s cheaper).

This and an initial investment can be set-up relatively quickly and once completed requires little to no maintenance allowing you to get on with your life safe in the knowledge your investments are compounding over time to produce returns you’re financial advisor would be envious of!