Erik Finman became a Bitcoin millionaire whilst still a teenager, Michael Burry made $2.69 billion betting against the housing market and George Soros made a tidy $1 billion betting so hard against pound sterling it almost bankrupted the Bank of England.

Investing is simple right? Just get it right once! Unfortunately, the media rarely presents the reality that betting big on single events is far more likely to lead to an empty bank account than a full one.

The truth is successful investing is far more monotonous than the newspapers have us believe. Yet over the long-term, it’s this ‘boring’ investing that can net us huge returns. Investing £350 a month and achieving a 7.5% annual return might not get you a featured in a film but start at 20 and keep going till 60 and compounded over time you’ll end up with £1,071,895.

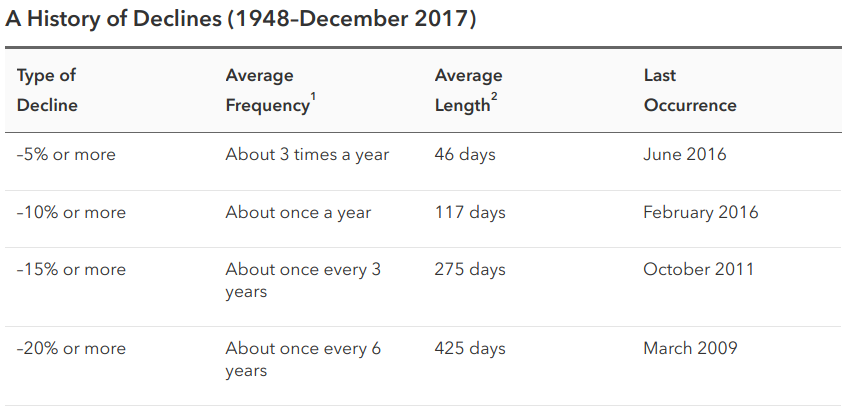

But what if one year from retirement the stock market plummets taking your one million down to £170,000 just like in the 1930’s? A 20% drop in your investments may be unacceptable, let alone an 83% drop!

Could you handle such a fall? How likely even is this? As covered in our recent post there has been a history of -20% declines about once every 6 years.

In order to reduce chances of large drawdowns (drops in investment value), many investors are content with returns that are less than what they could achieve if they had invested purely in riskier investments such as stocks and shares.

As any decent financial adviser knows, understanding your own risk tolerance is one of the foundations to set before starting to invest. This is where asset allocation comes in.

Asset allocation is the concept of balancing risk and reward by dividing your invested money across different investments (assets) to match your goals, risks and investment horizon.

So if you prefer a lower risk asset allocation, how is this achieved?

Reducing risk is achieved either by investing in assets that are lower risk and lower reward (such as Bonds) or by investing in assets with a negative correlation to each other. Meaning when one investment goes down another investment goes up.

In the 1800’s two English mathematicians developed a formula now known as Pearson’s R that scans two sets of numbers to tell us the correlation (=CORREL in Excel).

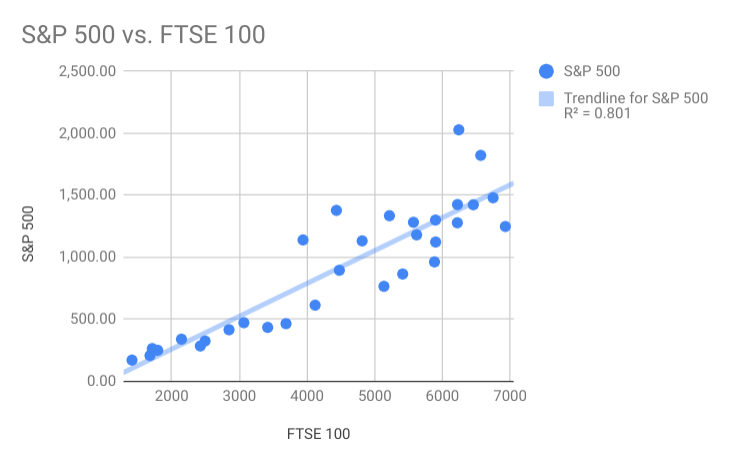

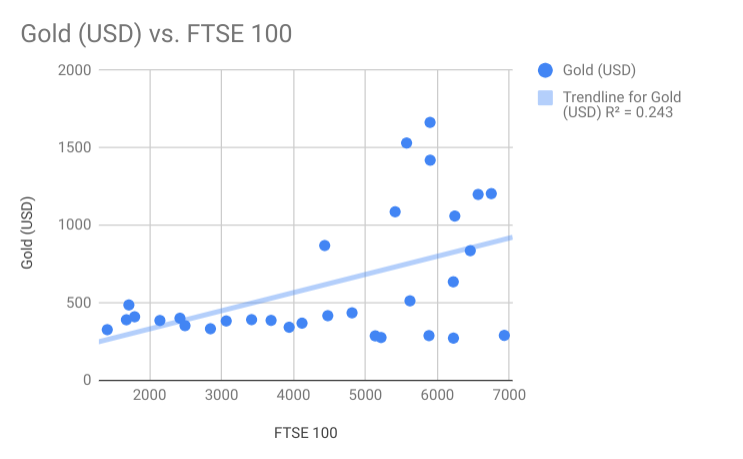

To give you an idea below are the correlations of popular investments between 1985-2015:

| Assets | Correlation |

| FTSE 100 & S&P 500 | 90% |

| FTSE 100 & UK Property | 73% |

| FTSE 100 & Gold | 49% |

Data for analysis: Only Gold – Gold price, Swanlow Park – FTSE 100 & Nationwide property index.

Or in visual format:

Note the linear line in the first example but randomisation in the second. As in the table, this demonstrates between 1985-2015 the FTSE 100 and S&P 500 were strongly correlated, yet the FTSE 100 & Gold were weakly correlated at best.

Understanding for example how the UK property market is correlated to the FTSE 100 may inform you that purchasing a property at an all-time high might a bad idea if the FTSE 100 has just crashed 80%.

Likewise, most stocks are highly correlated to their index so if our individual stock picks are going up in price, we may not be a genius we may just be benefiting from an overall rising tide. This also rings true in Cryptocurrency where most coins tend to be heavily correlated with Bitcoin. Hence during the Crypto Bull run of 2018 no matter what you invested in, it was likely to go up in price (and then down in 2018!).

As Warren Buffet once said: ‘Only when the tide goes out do you discover who’s been swimming naked’.

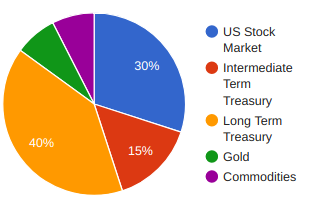

Below are three popular asset allocations backtested since 1972 using Portfolio Visualizer:

Ray Dalio – All Weather Portfolio

Annual return (CAGR) 6.33%, max drawdown 14.75%.

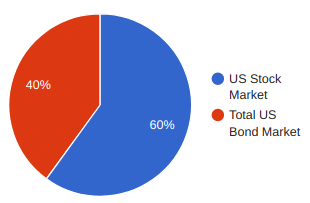

Classic 60:40 Stock and Bond split

Annual return (CAGR): 7.08%, max drawdown 30.72%.

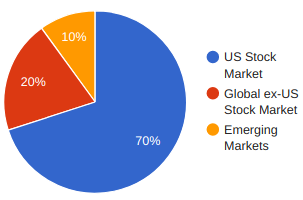

100% Global equities

Annual return (CAGR): 8.97% max drawdown 53.66%.

Typically the greater amount of volatility you’re willing to expose yourself to in the short-term the greater reward you can expect in the long-term. Hence the example portfolio with the highest return – 100% Global Equities at 8.97%, also had the biggest single drawdown (53.66%).

Identifying the most appropriate asset allocation for your own long-term goals, risks, and investment horizon is an incredibly personal question and one I simply can’t provide a broad answer for (nor am I legally allowed to!).

In discovering your own perfect asset allocation, you may want to ask yourself questions such as:

A Financial Advisor specialises in helping you answer these questions through the use of a tool such as Dynamic Planner.

As represented in the portfolios above equities tend to produce the highest returns and be the most volatile. However be aware over a long enough timeframe as in Game Theory any number of outcomes are possible. Because an investment has returned 8% a year historically, it does not mean it will continue to. Any outcome is theoretically possible.

Take 2008 as an example, over a 10 year period UK Government Bonds (Gilts) outperformed equities by 267% and in 2017 Gold and equities both produced double digit returns (Gold 12.81% & Equities 21.05%).

However, by allocating our money in a way that caters to our personal situation, we can expose ourselves to the best possible chance of achieving our personal goals.